Jumbo Home Loan

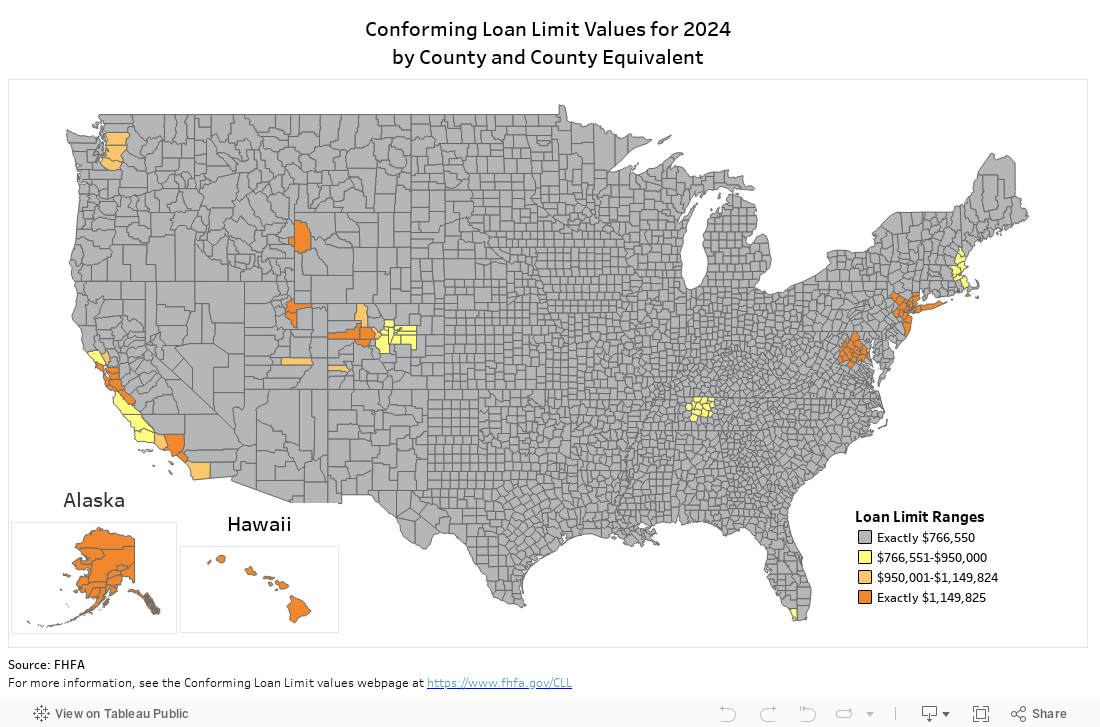

The table below shows conforming loan limits for all US and Colorado counties.

If you need to borrow more, consider a Colorado Jumbo loan.

What Types of Property Can You Purchase With a Jumbo Loan?

Since the government is not backing a jumbo loan, there are fewer limitations on the types of properties you can purchase using a jumbo loan. If you meet your lender’s requirements, you can use a jumbo loan for a primary residence, single-family home, investment properties, or vacation home.

-

Primary Residence

-

Single-Family Home

-

Investment Property

-

Vacation Home

Jumbo Mortgage Pros:

-

You can borrow more to purchase a higher-priced home.

-

Pricing for a jumbo loan can sometimes be better.

-

A reduced down payment as opposed to using a conforming loan limit and having to make up the difference in cash.

-

You can buy down rates (points) to reduce the rates.

Jumbo Mortgage Cons

-

Jumbo mortgages go through manual underwriting, which may mean you have more requirements to meet.

-

Higher borrowed amounts are riskier for lenders and this comes with higher rates or cash reserve requirements.

-

89.9 LTV (Loan to Value), but many lenders require a 15-20% down payment

What to Know About Jumbo Mortgages

How do Jumbo Loans Work?

Like a conventional mortgage, a jumbo loan will come with terms and a repayment schedule, but they work differently because private equity investors set the lending criteria. Some investors may be happy to lend against less demanding criteria but will charge a high premium in interest rate to offset the risk in doing so. Some investors may focus on cash reserves stored away.

-

Credit Score: Requirements will vary but typically 620 and up; it could be lower, but that will drive your rate up.

-

Debt-to-Income Ratio (DTI): Lenders will pay close attention to your DTI to ensure you won’t become overwhelmed by your mortgage payment.

-

Cash Reserves: Many jumbo loans want to see cash reserves. Borrowers must show they have enough reserves to meet the criteria; this amount will vary.

-

Closing Costs and Fees: A jumbo loan will have closing costs and fees similar to conventional ones.

-

Larger Down Payments: Jumbo loans commonly require a larger down payment of 20-25%, but this will depend heavily on the lender.

Does the Veterans Administration (VA) Offer Jumbo Home Loans?

Yes, VA does offer jumbo loans to service members who qualify. Generally speaking, jumbo loans are not backed by government mortgage programs, but there is always an exception to the rule, and in this case, it would be the VA.

VA Jumbo Loan Limits

Loan limits are based on the VA’s risk tolerance and the other limiting factor would be if the borrower had already partially used their VA benefit, reducing what they could qualify for on an additional home, if any. With a VA jumbo loan, it must be for your primary residence, not an investment property or vacation home. Property standards will apply to a VA jumbo loan.